Thoughtful reflections and insights on artificial intelligence

INDEPENDENT FINANCIAL COMMENTARY

THE 'GREAT' AI CON

How the biggest wealth transfer in history could end up in your pension fund

⚠ Not investment advice - read why this matters

The dot-com crash and the 2008 crisis were large. What is being constructed here - a concentrated AI bet baked into the default savings vehicles of tens of millions of people - has the potential to dwarf both.

The Rug Pull

AI is genuinely useful. Nobody serious is disputing that. What is being disputed or rather, what is being quietly ignored is whether the astronomical valuations being attached to AI companies bear any relationship to reality. We are watching the formation of the largest speculative bubble since the dot-com era, and this time the blast radius extends well beyond Silicon Valley into the retirement savings of ordinary people across the world.

The mechanism is straightforward once you see it. Venture capital funds loaded up early on AI at low valuations. Those companies now need an exit as AI is burning through money at an unprecedented rate. The exit is a public market IPO - and for that exit to pay off, retail investors, index funds, and pension schemes need to buy in at the elevated price. The risk, in other words, is being passed from wealthy insiders to everyone else.

The Rules Are Being Rewritten

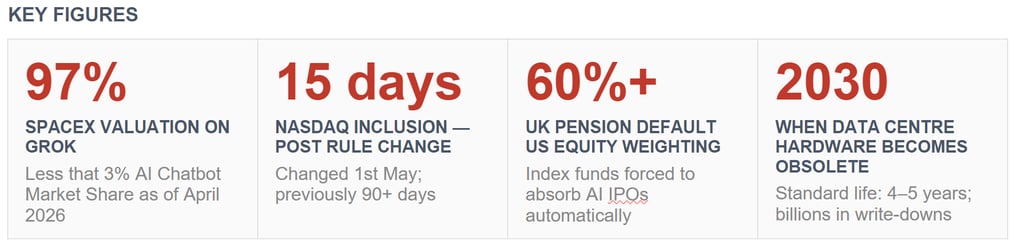

On 1st May, NASDAQ quietly amended the rules governing which companies can join its index and how quickly. Previously, a company would typically wait 90 days after listing before index inclusion. A cooling-off period that gave markets time to price shares rationally. The amended rules can see AI stocks join in as little as 15 days. The rules also reduced the percentage of stock required on the market and also increased the weighting multiplier methodology. All designed to facilitate the SpaceX IPO.

The practical effect: index funds are forced to buy at or near peak hype prices, with no time for the market to settle. This is not a neutral technical adjustment. It is a structural intervention that compresses the window between insider exit and public absorption.

When passive funds are mandated to buy a stock within a fortnight of listing, price discovery becomes meaningless. This is the mechanism by which risk is transferred from those who knew the price to those who had no choice.

The Prospectus Problem: SpaceX and the Grok Gamble

The SpaceX pre-IPO prospectus makes for extraordinary reading. Approximately 97% of the company's stated valuation rests on Grok - an AI platform that remains a niche product, used by around 2 in every 1,000 people worldwide, and which has attracted more headlines for generating non-consensual intimate images than for any breakthrough commercial application.

The prospectus gestures towards space-based data centres as a future revenue stream. This requires scrutiny. Rocket payload costs currently run at approximately $1,800 per kilogram. The economics of orbital computing do not remotely stack up against terrestrial alternatives. More telling still: SpaceX is not currently using its own AI infrastructure to full capacity and has leased spare capacity to rivals including OpenAI.

Three IPOs That Will Reshape Your Pension

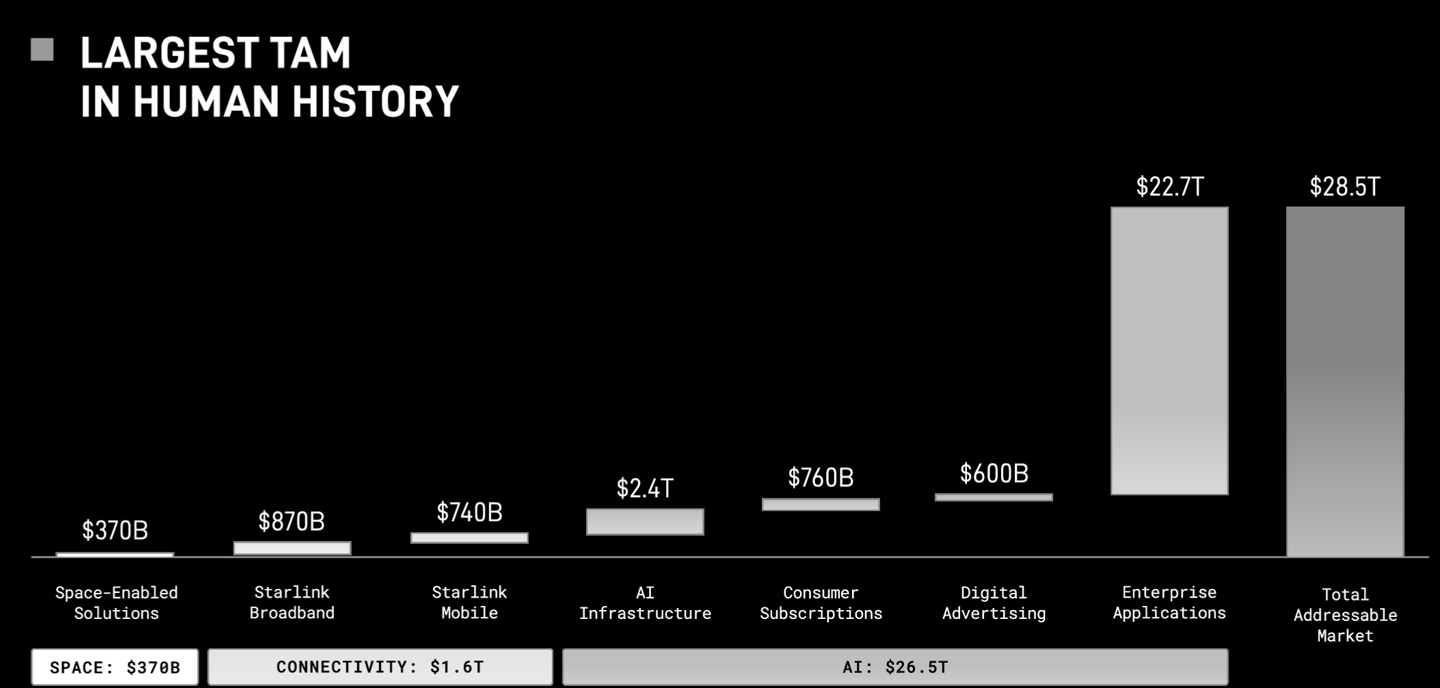

SpaceX, OpenAI, and Anthropic are each widely expected to rank among the ten most valuable companies in the world at IPO. Layer on top of that the existing AI exposure already embedded in Nvidia, Microsoft, Alphabet, and Meta, and a substantial proportion of any major equity index becomes a concentrated bet on AI valuations being sustained.

For American investors, this is primarily a 401(k) problem. For people in the United Kingdom, it manifests through defined-contribution workplace pension schemes - the default investment vehicle for the majority of working people since auto-enrolment. These schemes typically invest in index-tracking funds with more than 60% allocated to US equities. When AI stocks are added to those indices, the pension scheme has no discretion: it buys.

WHAT YOU CAN ACTUALLY DO

Practical steps before the reckoning arrives

▸ Do not buy into AI stocks directly on the basis of hype alone. Valuations are being set before commercial viability has been demonstrated. Wait for post-rationalisation when genuine business models become clear.

▸ Review how your workplace pension is invested. Most defined-contribution defaults are heavily weighted towards US index trackers. Understand what proportion of your pension is or will be exposed to AI stocks at IPO prices.

▸ Consider whether your pension scheme offers alternative allocation options with lower US equity exposure. Many schemes offer ethical, low-carbon, or geographically diversified alternatives that can reduce concentration risk.

▸ Treat AI IPO announcements with scepticism. The future may well be correct; the price may not be. Watch what venture capitalists are doing, not what they are saying. When insiders are selling, the exit is already underway.

It's all just a little bit of History, Repeating

Every generation has its bubble industry and its class of promoters - the hype merchants who rode blockchain, then NFTs, and have now seamlessly repositioned for AI. The playbook is identical: identify a genuinely transformative technology, detach valuation from any connection to present revenue, manufacture urgency, and ensure the exit occurs before the reckoning.

The dot-com comparison is instructive but insufficient. The scale here is materially larger. The structural pipes carrying the risk - passive index funds and workplace pension defaults - did not exist in the same form in 2000. The 2008 housing crisis spread contagion through mortgage-backed securities that most retail investors did not knowingly hold. This time, the exposure is explicit, visible, and inevitable for anyone with a workplace pension.

The Profitability Question No One Is Answering

No major AI platform has yet reported a profit. That is not a temporary growing pain it is a fundamental question about whether the current commercial model is viable.

The subscription-to-usage (token-based) pricing model, which enterprise customers are actively pushing back against, illustrates the problem. Token consumption is inherently unpredictable: a minor rephrasing of a prompt can produce significant variation in output length and cost. Newer reasoning models can consume tokens at twice the rate of their predecessors. Uber reportedly burned through its entire annual AI budget in four months, a cost profile that cannot be forecast, budgeted, or controlled in the way enterprise software spending normally is.

Disclaimer

This is independent commentary, not financial or investment advice. Nothing in this document should be construed as a recommendation to buy or sell any security or investment product. Readers should seek independent financial advice before making any investment decision. The author holds no positions in any stocks mentioned. Some of this content was generated with the assistance of AI.

What Happens When the Bubble Pops

History offers a guide. After the dot-com crash, the internet did not disappear. The underlying technology was real and transformative. What disappeared were the companies built on speculation rather than revenue - and the investors who had bought in at peak valuation. The survivors were those with genuine business models, even if it took years for those models to fully mature.

The same pattern will likely play out here. AI will transform industries, create new ones, and destroy others. The technology is real. But a significant rationalisation is coming, and the companies that fail will not be small names. The write-downs, when they arrive, will land on pension funds, 401(k)s, and ISA portfolios - because that is where the risk has been transferred.

Contact

Questions or thoughts? Reach out anytime.

Contact us:

© 2026. All rights reserved.